Agentic AI Drives Structural Expansion in Memory Demand, Global Memory Market Projected to Reach US$1.28 Trillion by 2027, Says TrendForce

The shift in AI development from large-scale model training toward inference-centric Agentic AI applications is driving a structural expansion in memory demand, according to TrendForce's latest findings on the memory industry. With the resulting supply deficit unlikely to be resolved in the short term, prices are set to rise further.

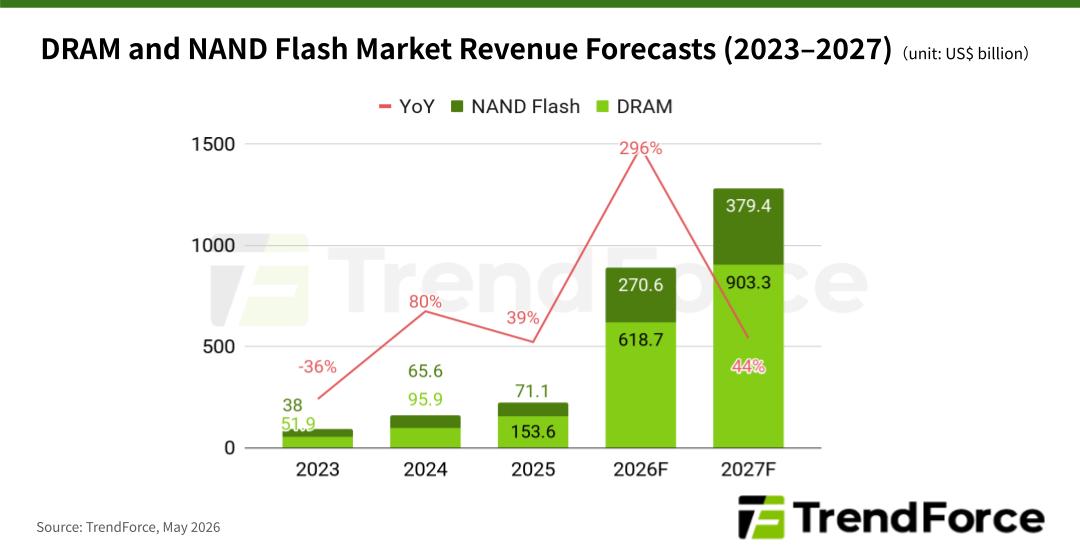

TrendForce has therefore significantly raised its global memory market forecasts, increasing its 2026 estimate from US$551.6 billion in the previous report to $889.3 billion. Meanwhile, the 2027 forecast has been revised upward from $842.7 billion to more than $1.28 trillion, representing annual growth of approximately 44%.

DRAM demand trends indicate that inference requests in Agentic AI systems are evolving from single queries into continuous iterative cycles. Furthermore, KV cache capacity is scaling proportionally with larger context windows. If recalculation is required, compute costs will increase exponentially. As a result, efficient KV cache management has become critical to AI inference performance, directly driving demand for HBM and DRAM.

Agentic AI workloads are significantly increasing CPU requirements for scheduling, data preprocessing, and memory management. In next-generation AI server platforms, CPU-to-GPU ratios have gradually shifted from the traditional 1:8 toward 1:4 or higher. For example, NVIDIA’s NVL72 rack adopts a 1:2 configuration. This means rising CPU deployment is expected to expand server DRAM capacity requirements while simultaneously supporting procurement volumes and contract pricing.

Additionally, the growing wafer consumption associated with HBM production is compressing available capacity for conventional DRAM. Under expanding demand conditions, this further strengthens suppliers’ pricing power in contract negotiations, with upward pricing momentum expected to extend through 2027.

TrendForce therefore raised its 2026 DRAM market forecast to $618.7 billion—representing annual growth of 303%—while 2027 revenue is projected to further expand to $903.3 billion, up 46% YoY.

In the NAND flash sector, combined capital expenditures from the world’s nine largest CSPs continue to rise rapidly, with 2026 growth projected to reach 79%. Capital intensity is also expected to increase to 34%, reflecting a strategic shift from demand-driven capacity expansion toward large-scale AI infrastructure investment aimed at securing long-term competitive advantages.

The underlying driver is likewise Agentic AI. AI agents are significantly increasing enterprise usage, with heavy users consuming up to four times more tokens than before. At the same time, the growing complexity of AI-generated media content is substantially accelerating token consumption.

Facing massive and continuously rising memory demand, HBM remains too costly for broad deployment at scale, while HDDs are constrained by access speed and limitations on power consumption, making them unsuitable for real-time AI data center workloads.

This dynamic is creating significant growth opportunities for NAND solutions. From SCM SSDs and HBF to SLC/pSLC SSDs, a wide range of high-performance SSD technologies are rapidly penetrating AI inference, training, and agentic workloads across multiple layers of the ecosystem, emerging as key growth drivers.

NAND flash pricing remains resilient thanks to strong demand and constrained supply. TrendForce has revised its 2026 global market forecast for NAND flash upward to $270.6 billion, representing annual growth of 280.7%. The 2027 market is projected to further expand to nearly $379.4 billion as it maintains a strong annual growth of 40.2%.