Long-Term Agreements Cap Price Increases; Server DRAM Contract Prices Expected to Rise 13-18% QoQ in 3Q26, Says TrendForce

TrendForce’s latest memory pricing survey indicates that multiple memory suppliers have already factored in expected price hikes into their prices for the second quarter of 2026. Additionally, several U.S.-based CSPs have entered into multi-year long-term agreements (LTAs), which restrict suppliers from raising prices for these clients.

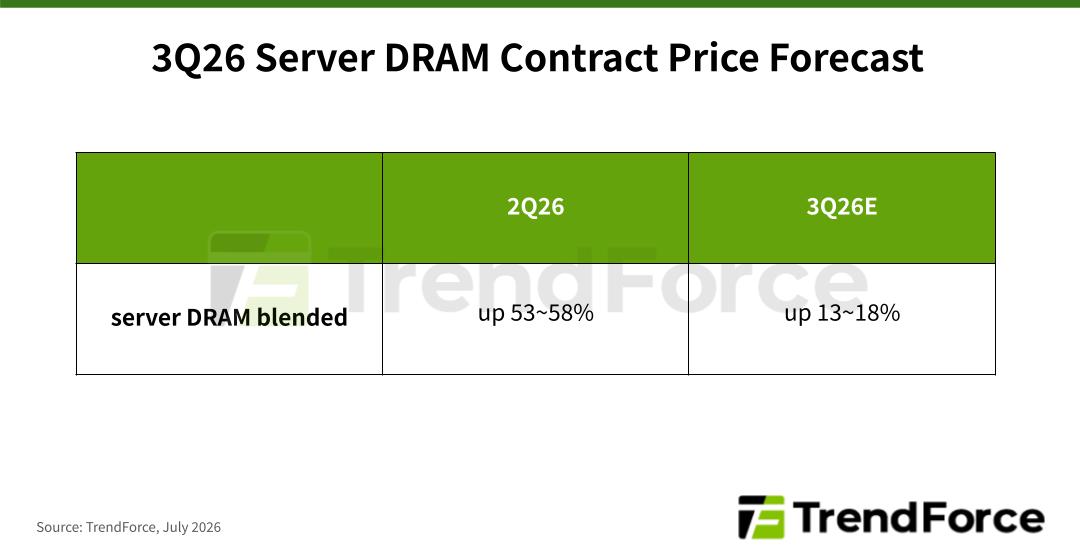

Consequently, TrendForce predicts that server DRAM contract prices will rise by 13–18% quarter-over-quarter in 3Q26. However, as the market remains undersupplied, memory suppliers may continue revising quotations upward throughout the remainder of this quarter.

TrendForce notes server CPU shortages have slowed system assembly, leading to a gradual buildup of DRAM inventories at U.S. CSPs during the second quarter. CPU supply is expected to improve progressively from the second half of 2026 through 2027, allowing server production to ramp up. Meanwhile, a server DRAM shortage is already anticipated for 2027. Against this backdrop, CSPs continue to increase procurement to prepare for future demand.

During the latter part of the second quarter, major memory suppliers began providing customers with preliminary supply guidance for 2027. TrendForce’s initial estimates predict that total RDIMM bit supply will grow by only 15–20% YoY, significantly lagging the projected growth in server CPU shipments.

As a result, even buyers that have already secured sufficient supply for the second half of 2026 still have a strong incentive to build inventory in anticipation of the tight supply conditions expected in 2027.

Given that some CSPs have already entered into long-term supply agreements, TrendForce expects that beginning in the third quarter of 2026, the primary source of server DRAM price increases will shift toward customers without LTAs, as well as incremental supply sold outside LTAs to existing LTA customers.

Overall, server DRAM contract prices are expected to continue rising quarterly from the second half of 2026 through the second half of 2027, although the pace of price increases is likely to moderate.

The changing mix of server memory module capacities also reflects customers’ efforts to control procurement costs while aligning purchases with CPU availability. Since the first half of 2026, CSPs and OEMs have gradually adjusted their RDIMM configurations, with some systems shifting from 96 GB and 128 GB modules to 32 GB and 64 GB modules.

TrendForce expects this transition to become increasingly evident in suppliers’ shipment mix starting in the third quarter. This will result in quarter-over-quarter growth in shipments of lower-capacity modules while slowing the previous decline in their share of total bit shipments.

The memory market watcher

DRAMeXchange is a global primary provider of future intelligences, in-depth analysis reports and advisory services on DRAM and Flash memory industry with coverage including current business, spot trading prices, and market trends, capital spending and wafer capacity trends, the impact of DRAM/flash memory products on the market, and other relevant PC industry information.

© DRAMeXchange ® Tech.Inc. All rights reserved.