Global Smartphone Production Fell 1.7% YoY in 1Q26; Memory Cost Pressures Expected to Drive a Sharper Decline in 2Q26, Says TrendForce

TrendForce’s latest figures reveal that global smartphone production reached around 284 million units in the first quarter of 2026, marking a 1.7% YoY decline. Despite a sharp rise in memory prices since the second half of 2025, the effect on production was minimal because brands still held inventories of cheaper memory components. Additionally, consumer expectations of higher prices in the future have helped sustain short-term demand, cushioning the impact of rising memory costs on production during the quarter.

However, as low-cost memory supplies are gradually exhausted and significant ongoing increases in memory prices reduce profits, most smartphone brands have begun adjusting production in the second quarter.

Looking ahead, TrendForce forecasts global smartphone production to decline approximately 16.2% YoY to 1.051 billion units in 2026. Under a more severe scenario, the annual decline could become even more pronounced if memory price increases remain elevated and brands are forced to raise retail prices repeatedly.

Smartphone vendors are adopting different strategies to overcome the challenges. For instance, brands with strong premium pricing power and broader group-level financial resources are more likely to maintain or expand market share. Meanwhile, Chinese brands focused on the mid-range and entry-level segments are following more conservative production plans due to mounting pressure from rising costs and intensifying competition from Huawei.

Diverging strategies across brands; Samsung, Apple, and Huawei poised to grow against the trend

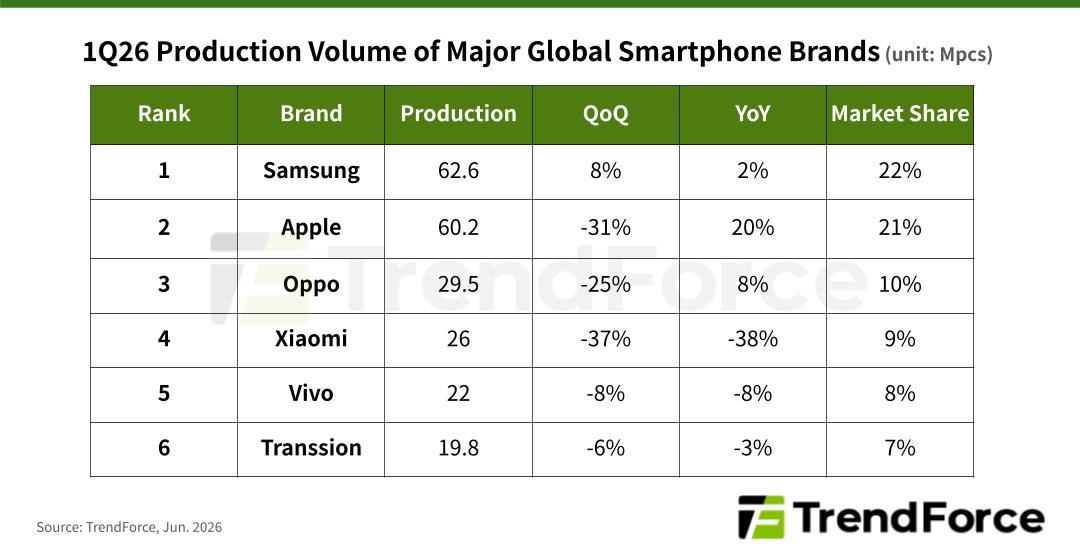

Samsung remained the world’s largest smartphone producer in 1Q26, with output reaching approximately 62.6 million units. Production increased 7.6% QoQ and 2.3% YoY, supported by inventory build-up for new Galaxy S-series models.

TrendForce notes that Samsung is relatively well-positioned to withstand the current cost inflation cycle thanks to strong financial backing from the broader Samsung Group and a sizable premium product portfolio. Nevertheless, its significant exposure to lower-end models remains a concern—particularly amid weakening consumer sentiment—making end-market demand a key factor to monitor.

Apple ranked second with its production of approximately 60.2 million units during the quarter. In addition to ongoing production ramp-up for new iPhone models, output was supported by the launch of the iPhone 17e, resulting in 19.7% YoY growth.

Compared with competitors that have already entered a margin-protection phase, Apple remains better positioned to absorb higher memory costs while maintaining profitability. TrendForce believes Apple is more likely to prioritize market share expansion during the current downturn as it lays the groundwork for future growth in recurring software and services revenue.

Xiaomi, Oppo, and Vivo focus on preserving profitability as production plans face greater uncertainty

First quarter production declined seasonally among the major Chinese smartphone brands, including Oppo (29.5 million units), Xiaomi (26 million units), and Vivo (22 million units). These three brands ranked third through fifth globally by production volume.

While all three delivered strong market share gains in previous years, surging memory costs are now weighing heavily on profitability, creating significant uncertainty around their 2026 production plans. As a result, production targets may be revised downward if cost pressures persist.

Transsion produced approximately 19.8 million units in 1Q26, roughly flat compared with the same period last year, placing sixth among global smartphone brands.

The brand has been particularly vulnerable during the current memory price supercycle given its smartphone portfolio is heavily concentrated in entry-level and budget segments—where profit margins are already thin. Limited access to low-cost component inventories has further amplified the impact.

Nevertheless, demand from emerging markets continues to provide an important source of support for the global smartphone industry. As competitors such as Xiaomi scale back production of lower-end models, Transsion may benefit from residual demand in price-sensitive markets.

The memory market watcher

DRAMeXchange is a global primary provider of future intelligences, in-depth analysis reports and advisory services on DRAM and Flash memory industry with coverage including current business, spot trading prices, and market trends, capital spending and wafer capacity trends, the impact of DRAM/flash memory products on the market, and other relevant PC industry information.

© DRAMeXchange ® Tech.Inc. All rights reserved.