Rapid Contract Price Surge Drives 1Q26 DRAM Industry Up 81% QoQ, Says TrendForce

TrendForce’s latest survey reveals that the memory industry experienced a significant boost in 1Q26 due to rapidly rising contract prices for conventional DRAM, which increased by approximately 93% to 98% QoQ. This surge contributed to an overall industry revenue increase of 81% QoQ, reaching $97 billion.

As AI applications evolve from focusing on LLM training to AI inference, CSP data centers are shifting their deployment priorities from AI-specific servers to general-purpose servers. This shift is expanding memory procurement needs beyond just HBM3e, LPDDR5X, and high-capacity RDIMMs to include RDIMM products with a broader range of capacities.

In the second quarter, inventory levels at DRAM suppliers remain extremely low, while incremental supply is prioritized for high-capacity RDIMMs for AI servers. This limits product availability for PC OEMs and smartphone vendors. As a result, bit shipment growth for conventional DRAM is expected to remain constrained.

On the pricing side, CSPs have shown a greater willingness to accept price increases, which has prompted other customers to follow suit to secure supply allocations. TrendForce therefore expects conventional DRAM contract prices to rise another 58–63% QoQ in 2Q26.

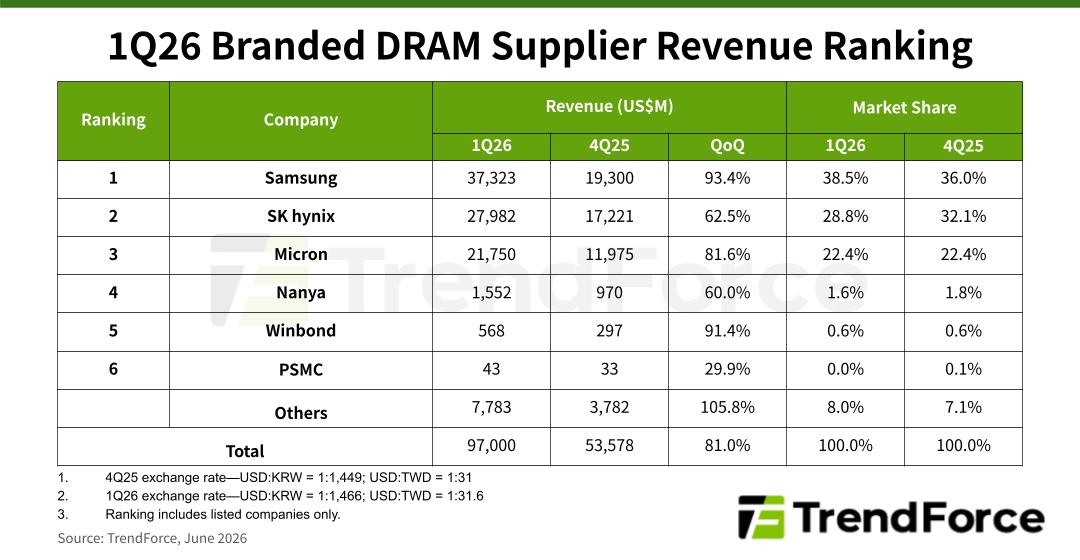

Samsung retained its leading position in 1Q26, benefiting from the strongest ASP growth among the top three DRAM vendors. The company also maintained the highest server DRAM revenue contribution, driving quarterly revenue up 93.4% QoQ to $37.32 billion and increasing market share to 38.5%.

hynix, which recorded the highest HBM bit shipment mix among the top three suppliers, saw overall ASP growth partially constrained by declining HBM contract prices in 2026. The company posted 1Q26 revenue of $27.98 billion, up 62.5% QoQ, ranking second with a 28.8% market share. Micron ranked third, with quarterly revenue surging 81.6% QoQ to $21.75 billion, while maintaining a stable 22.4% market share.

TrendForce notes that the upward momentum in conventional DRAM contract prices persisted throughout 1Q26, with the top three suppliers continuing to prioritize production and shipments toward higher-priced, higher-margin server applications.

Suppliers are expected to rely primarily on process migrations to expand bit output in 2026, given the increasingly tight supply environment and the time required for new cleanroom construction. Meanwhile, wafer input growth will remain limited to incremental gains achieved through manufacturing optimization.

Taiwan-based suppliers Nanya, Winbond, and PSMC continue to focus on mature-node DRAM products to fill market gaps left by the top three suppliers as they transition toward advanced process technologies. Nanya significantly reduced inventory during the quarter, while sharp increases in DDR4 and DDR3 contract prices drove revenue up 60% QoQ to $1.55 billion.

Winbond expanded shipments of DDR4 and LPDDR4 products in 1Q26, lifting quarterly revenue 91.4% QoQ to nearly $568 million. PSMC’s revenue from its internally produced consumer DRAM products rose 29.9% QoQ to $43 million, while total revenue, which includes foundry operations, increased 19.3% QoQ. Following its licensing agreement for Micron’s process technology, PSMC is expected to aggressively expand supply capacity going forward.

The memory market watcher

DRAMeXchange is a global primary provider of future intelligences, in-depth analysis reports and advisory services on DRAM and Flash memory industry with coverage including current business, spot trading prices, and market trends, capital spending and wafer capacity trends, the impact of DRAM/flash memory products on the market, and other relevant PC industry information.

© DRAMeXchange ® Tech.Inc. All rights reserved.